![]()

Quick Tips for Logistics Professionals

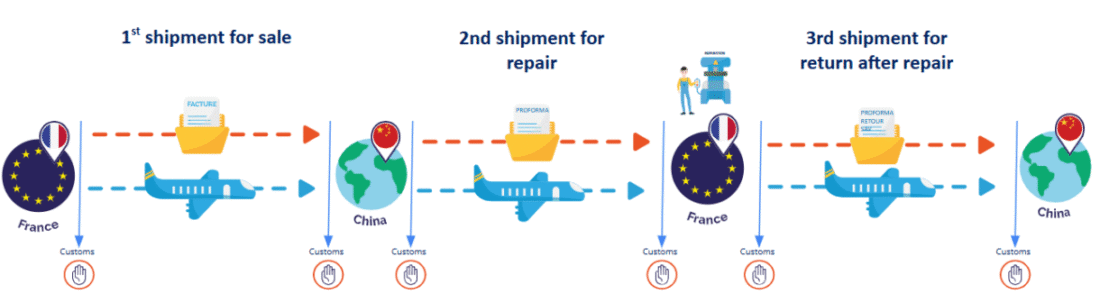

- International after-sales returns involve several customs procedures (initial export, re-import, re-export after repair, final re-import).

- Three customs solutions for your after-sales returns:

- The Return System (RGR) customs procedure for returns is suitable for one-off flows, but requires precise documentation (serial numbers).

- It’s easy to release for consumption, but there are tax risks (non-deductible VAT).

- Inward processing is ideal for regular, complex flows (high value, high rights).

- Successful returns depend on the quality of customs documentation (invoices, serial numbers, reasons for return).

- Beware of flows managed by express carriers : give preference to a Registered Customs Representative (RDE).